A former Red Rock auto dealership employee contacted AnneLandmanBlog wanting to unload about what he experienced in the years he worked for the dealership. He asked to remain anonymous, so his name is withheld. He said he was “ashamed” about having worked for the dealership and wanted to do whatever he could do to help people who fell victim to these scams.

Following are excerpts of our conversation, edited slightly for clarity:

——————-

Q: Thanks for agreeing to talk with me. What did you do at the dealership when you worked there?

A: I did a little of everything. I was Service Manager, sold cars, did a little of everything.

Q: So, what’s on your mind about working for Red Rock?

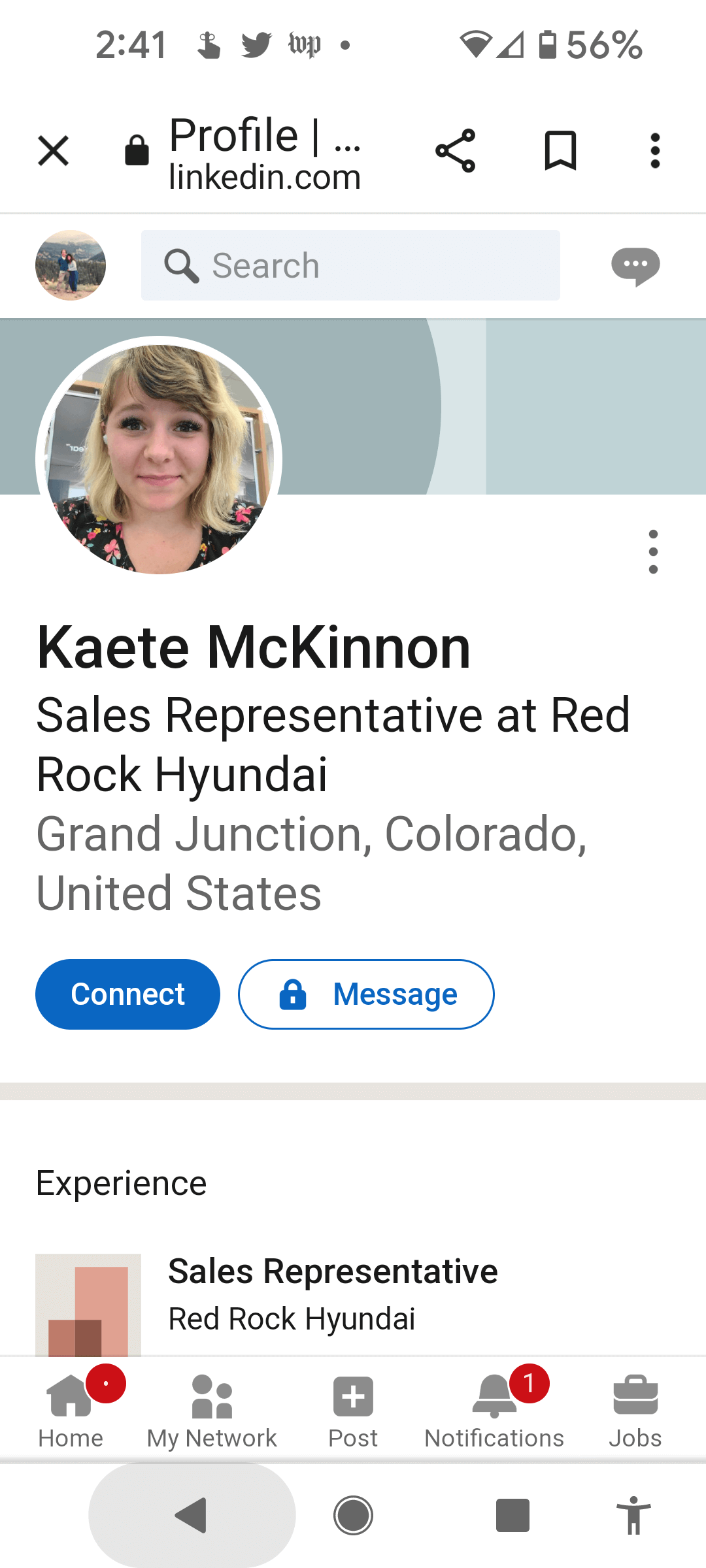

A: So, basically that one customer with the truck, where he claimed they forged his signature? I worked there when that happened. The employee who actually forged the signature still works at [Red Rock] Hyundai, her name is Kaete … And then the finance manager that had her forge his signature for the warranty took the fall for her and he left. He’s actually working at Carville’s now, so I mean that’s just it. There’s a lot of shady stuff like that, like with the iPad [they use] to just screw as many people they can. They undervalue trades, they call it “ripping the trade.” They get paid commissions off what they sell warranty-wise, gap [insurance], ResistAll, Covid spray… So whoever got the Covid spray, they never did anything for Covid Spray. [The customers] got ripped off because they really don’t do anything for that.

{kind=link}

{kind=link}

Red Rock Hyundai, 2162 Highway 6 And 50, between Fruita and Grand Junction

Q: So how does management communicate to salespeople how to swing these iPad signature deals, where they have people sign on an iPad, and then populate the signature lines without showing the contract to people before they leave the dealership. How do they teach people to do that?

A: I have no idea. I mean, I only worked there for a few years and the guys had been there long enough that whoever taught them, I’m assuming it’s a trick of the trade, I would guess.

Q: It seems to be peculiar to the Tim Dahle-owned Dealerships…

A: Yeah, because I bought a car at ******* and [they do] the iPad stuff too, but they outlined and walked me through everything, including the warranty, what the cost was, how long the warranty was…

Q: What percentage of customers typically fall for this iPad trick?

A: I’d probably say, most of them. I’d say, 80-90%, because they falsify stuff to the bank. They lie about people’s income to get deals funded. There’s a whole slew of stuff that they do.

Q: How does this falsification of financial information work?

A: So, for example say someone comes in, they’re interested in a car and they make $1,000/month on Social Security. Well, obviously most banks won’t loan to someone like that on a car with a $300-$400 payment. So they’ll say, “Oh she makes $5,000 a month as a secretary or an administrative assistant,” or something like that. So when they submit it [the financial information] to the bank…They have an internet program they use to submit information to the bank that everyone in the country uses called “CUDL,” so they modify that information and then .… It’s called “bumping their income.”

Q: So, they’re lying to the banks, then, right?

A: Yup, yup, oh yeah, oh, yeah.

Q: Do you still work for them?

A: No, no, I quit … because they asked the people to lie. I’m not going to lie, and so I left.

An example of a “Four Square” sheet, a disreputable sales tactic that dealerships have used for decades to confuse customers and get them to agree to a deal that advantages the dealership. By constantly scribbling different numbers, moving numbers around, making different lists and using different pens, the salesperson can easily confuse customers and make it look like they are getting a good deal when that isn’t the case.

And another that thing they do… When people say “They closed me on a payment twice as much as I can afford,” like the one article you have, they probably have a warranty included [in the total price on the contract], and that’s why it was so much… They call it a “Four Square.” When they [salespeople] present the numbers [to the customer] they say “O.K., here’s what the car is worth, here’s what we’re going to give you in trade, here’s your downpayment, and this is what your [monthly] payment would be. Sign if you agree to it.” So they don’t give you any numbers of what they’re giving you for trade value, they don’t give you any numbers unless you ask for it…So if just sign your name, and say you go in there with a $400 payment max, and then you come out and sign on an $800 payment, which a lot of people do, then they don’t show you. They just take you to the back and have you sign the paperwork and you’re good to go, which always includes the warranty and stuff.

It’s interesting [because] their dealerships don’t work like most dealerships do. In most of my dealership experience, the finance people have to sell the warranty. When you talk to the finance guy before you sign the paperwork, they say “Hey before we sign this, I just want to offer you this [extended warranty] on your car, here’s the cost, here’s the years, here’s what it covers…” That’s not how Red Rock and the Tim Dahle do it. They have the salespeople close [the customers] on a payment, and that high payment includes everything.

Q: Oh, so that’s why people don’t know what’s included. They’re only looking at the monthly payment.

A: Yup, exactly.

Q: So, I am in touch with a couple who … said they have never seen the contract. They got handed their documents on a USB drive.

A: Yup, that’s what they do, that’s what they do there.

Q: I guess maybe not everybody has a…

A: …a computer that can use a USB drive.

Q: Yes.

A: Well, that’s why the best thing I can suggest is for everyone to ask to get your stuff on paper. Ask for paper on everything.

————–

This gentleman also remembered one couple who finally saw their contract after leaving the dealership and saw Red Rock had charged them an extra $6,000 for “paint protection.” They came back to the dealership angry.

His boss blamed him for the charge.

He added, “If people reach out I’m willing to help and do whatever I can to help.”

#FraudRock

As a Former Employee of the Tim Dahle Auto Group in Utah. I have zero ties to the Red Rock Dealerships but I can attest to the Tim Dahle Auto group and the shady practices they teach and preach from the owners on down.

I worked in their service department for a few years at a few different locations in the service department. The first clue I got that things were shady was when I would have customers come in with having purchased what they were told was an all inclusive extended warranty. The sad part is most of these customers would come in having spent thousands on extended warranties that were not mechanical contracts they were electronic component warranties.

I had the task several times to try to correct extended warranties so that customers had the correct warranty. This is just the start to the shady practices preached at the Tim Dahle Auto Group.

The next red flag was when they asked us in the service department to start selling everything as an all inclusive price. Stop quoting labor and parts separate. Why you might ask it’s because they have a grid system that they do not inform their customers of. Let me explain how this works. For every hour you pay for a repair or book time for the tech so say the job pays 4 hrs. The dealership door rate per hour is $185. Well for every hour that job pays it goes into a grid system and instead of 4 hours at $185 you are now paying $205 an hour on the grid. They use this on every service customer.

The sad part is I have seen them overcharged service customers daily and most transactions are a few hundred dollars extra but I have seen them charge $1000’s more than the door rate. Not to mention the mark up from their parts department is a joke.

The final shady practice that their dealerships all participate in which was fraud in my eyes. They sell you an extended warranty but when you come in for a repair they ask the manufacturer for good will assistance, then they double charge the extended warranty. This part saves the customer the deductible but it fraudulently takes money from the dealerships.

So, if I was a customer or former customer of their service department and you paid out of pocket for service in the last 3 years. I would call another place find out what the book time was for the repair then compare it versus their door rate. If it’s higher I would go in and mandate a full refund.

If I was a manufacturer especially a Nissan I would audit every single repair order the dealership has. When I brought these issues up to the Service Manager and GM I was told by both if I didn’t like it once I left their office I could keep walking and pardon my French but I could keep walking out the “fucking door” and work somewhere else. I decided at that point it was not a company I wanted to be associated with and left

As someone in the automotive industry, but not a dealership, this sounds like someone with a bone to pick, spurning his or her former employer. Are there shady people and shady dealerships? Absolutely. Are some of the accusations made feasible? I suppose so….but reading through the comments it seems like someone who really doesn’t understand what is happening. I have worked at a dealership in sales, F&I, and at multiple different software companies who help dealerships drive business (CRM, Websites, Marketing, Service Scheduling, etc) for the past 6 years. I’ve consulted thousands of dealerships. No doubt there the industry has a bad name because of a few bad actors – particularly from the 80s to early 90s, but looking at these comments I could easily go through each claim one at a time and dissect it to find inconsistencies and highlight how there is probably an agenda driven narrative. I say this as someone who has ABSOLUTLY ZERO TIES to Red Rock Hyundai. I don’t know a soul there. I have never even spoken with them – so I do concede that some of the claims are POSSIBLE – but most of this is very likely not below the belt dishonest treatment as being ascribed. For example, take the comment about ripping people off using ipads – there is zero detail about it. He first claims they devalue trades – well, duh! Is there anyone alive who doesn’t expect a dealership – who takes on hundreds of trades a month with a short inspection, and gets bit on 3-4 of them with major issues that weren’t obvious in a 5 minute appraisal – to pay top dollar for every single trade? No, they try to offer as little as possible to ensure they stay profitable and stay open. Maybe they will make $1500 on one trade and $2000 on another, but then they lose $1800 on another. No one can make a customer take a trade offer. If it is worth it to them for the convenience of not having to sell it or pay it off on their own first, then they will pay a premium and can negotiate with the dealership for it…but trying to, as the author put it, “rip” a trade is not a dishonest practice. The complainer then makes more claims about the ipad without giving detail. I’ve worked with hundreds of dealers and have never seen a customer finalize a deal without getting a copy of the paperwork. If it’s on a flash drive, they can ask for a printout or view it on a computer first….they have to sign a doc to finalize a loan with the credit union or bank and they always get a copy of that (CUDL is just a portal that connects to thousands of credit unions where they can securely transmit someone’s information for a loan, another one often used is Dealertrack). The claimant then, when asked for more details about how the ipads are used fraudulently says, “I have no idea….I only worked there for a few years….it’s a trick of the trade….” Zero to support a claim about shadiness, just “trust me, I’ve seen it.” Then he/she goes on about a four square….which is a tactic many dealers use to come to terms with vehicle price, trade in value, down payment and monthly payment. Yes, they want to get someone happy with a payment, mostly because that is THE MOST IMPORTANT THING TO 90% OF CAR BUYERS….It is also a way to help them make some profit. Oftentimes dealers will take a loss on a deal “front end” because they will be able to make some money on a warranty, or gap insurance, or interest from the bank/credit union. Here is where payments are mutually beneficial. If a deal is a “no sale” to a dealer because the margin is too low, but the customer buys a 1200 warranty that costs the dealer 600 wholesale, then the customer gets a car at a payment that makes sense to them, while the dealer closes a deal that makes sense to them. Without that “back end” profit, the dealer just says no and it’s a lose-lose instead of a win-win. Now, can savvy consumers do the math and figure what their payments will be based on the trade, down payment, car price and loan terms – absolutely…but dealerships seeking to make a modest $2000-4000 profit on a $40,000 vehicle is not unreasonable. Most commodities have much more than a 5-10% markup. There is a lot of expense that goes into running a dealership, and that is spread across every car deal….so using a 4 square tool that helps both parties meet in the middle is also not dishonest.

I’ve spent way too much time on this – but to sum up, the author and interviewer both seem to have very little experience and understanding of the industry. I would venture to guess that there might be some truth to the story, but the dealership is probably immensely better than they are characterized and there is probably a lot of either misunderstanding or sensationalization to the story.

Thanks for your insight…very interesting stuff. Bottom line, the buyer and seller are in an adversarial relationship and the buyer should know that. However there is a desperation aspect to this in the event of the buyer being short on cash. Lots of flim-flamming can take place at this juncture.

I posted something early on in this thread about the iPad. We went into the finance guy’s office and he tried to sell us upgraded warranties, which we refused.

This was a cash deal with no trade in and we commenced to “sign” the papers.

It wasn’t until we got home that I saw two charges for things that hadn’t been explained to us and we didn’t want. I called immediately and they gave us a fight about a refund. But I stood firm and got it. Truth be told, I don’t even know if we signed up for these services. They could easily have forged the signature.

PS Do you know what the typical mark up is on a used vehicle?

We were told their price was as low as they could go but I had no idea what they had actually paid for the vehicle.

I suppose if you walk away and they really want to sell it they might come down.

It’s a lot about the bluff, which is why I hate buying cars.

There really isn’t a “typical” markup. It varies by make, model, body type (truck vs suv vs car), region, dealer group, etc. The “Average” gross profit on a car pre-covid was 1500-2000 front end and another 500-1500 backend (warranty, gap, rate points, accessories), so typically 2000-3500 per car, with an average sale price of 25k. They have to pay sales reps, f&I, and all dealership operations out of that.

With Covid that “average” jumped up about 3500-4500 front end and 1000-1500 back end, so a total of about 4-6k, but vehicle cost also grew by about 1500-2000 and volume plummeted so far more margin to keep the dealership operational came out of each car. Front end gross profit is just now beginning to decline significantly, to about the 2500-3500 range….but again, it varies. A big truck or Escalade/Suburban could have a 6-8000 profit, whereas a Chevy cobalt or Ford focus might have a 1200 margin – almost nothing for the dealer to operate with and stay afloat.

Most good dealerships are focusing on profit per day for vehicles. It’s better to make 3000 on a car that moves in 15 days than 9000 on a truck that moves in 60 days, because they could sell 4 cars and make 12k total during the time they sold 1 truck for 9k….this means that a dealer is motivated to move aging inventory. They might turn down an offer that makes them 3500 today, but if that car is still around in 60 days they will sell it at a loss, just to free up their capital to buy other, more profitable vehicles….one dealer might focus on high quality cars and hold their margins, while another dealer might focus on being the low price leader and target fast turnaround and volume….so it really is hard to give a “typical” markup.

Thanks…it’s what the market will bear.

One salesman told me I might get a better price if I financed but when I asked what the interest would cost, they did drop the price slightly because I planned to pay off the loan right away.

They get a kickback from the lender.

Lots of moving parts!

What I did was research the vehicle/mileage we wanted in the area (including Utah and Nevada. We were in the ballpark so I figured we did as well as possible.

Glad we’re over all this. Not fun at all!

As a current employee of Red Rock Auto Group this saddens me. I think that things have been misconstrued in many ways. I have NEVER been asked to do anything shady and they have been nothing but good to me in the over 3 years I’ve been with the company. I think people should also take into account that Red Rock Auto Group employs over 250 people here in Grand Junction, supplying families with an income. I have seen Red Rock Auto Group send several mechanics and Lube Techs to school to get certified, furthering their knowledge and careers.

They also acknowledge employees for their hard work giving raises, promotions and bonuses often. I’ve had family members and friends purchase vehicles from Red Rock Auto Group with no problems at all. I personally feel like they’re my 2nd family, I love everyone in the group. Red Rock Auto Group sponsors sports teams, non profits and even a Lego team. I’m not sure if anyone saw or would like to recognize the $20,000 given to Roice-Hurst Humane Society by Red Rock Auto Group and their employees last month. RRGJCO has helped countless families in need and doesn’t seek recognition. Red Rock Auto Group allows and encourages employees volunteer (on the clock) at the Catholic Outreach Soup Kitchen twice a month for almost two years now. They truly believe in giving back & continue to do so. In fact, I know they are about to do something really big for another nonprofit here in Mesa County that will be invaluable to the organization. I urge you to keep an eye out for that too. I should also tell you that at our group employee meetings we are always reminded that without our customers we wouldn’t be here and to treat them as our own family.

Anyhow, I’m not here to argue or anything along those lines, just here to bring another point of view from an employee of Red Rock Auto Group and shed some light on the positive they are doing for our community.

I hope my comment doesn’t get removed and I would be fine with Anne contacting me with any questions. I also want to add that nobody has asked me to write anything, this comes straight from my heart.

Much love to everyone and I hope you think twice before jumping on the negative train.

Still doesn’t take away that maybe not you but the tons of people that have been taken for thousands of dollars or put into a financial bind because your group of dealerships! It may not be you specifically but your group are definitely taking advantage of people. Must be nice to make those donations when you’re taking tons of money from the community you say you guys care about!

I also worked for the Red Rock Group and I Had to leave. Working there went against everything I believed in. The amount of people that walked in everyday pissed off because they got sold a BS warranty that doesn’t cover anything is INSAINE!!! I have personally seen managers including GM of the store laugh at people after they came in and expressed their anger towards what they where sold. They would promise to call back and fix things and never would. Everything from the GM to the Techs is a joke. A lot of Stress is put on everyone that works there. Every single person that works for RRGJCO has said them selves they would never buy a car from them. That says a lot if your own employees wont even buy a car from you because they know what these dealerships are about. I Hope they get shut down they have done a lot of damage already thy don’t need to make more.

The dealerships in Jct are aware of this blog & the Facebook discussions. I’ve been called to assure me that my business is appreciated and the pricing of my needed work is accurate. Hope that’s correct!

I hope the District Attorney is interested in your research.

He is. The Mesa County D.A. has referred the case to the CO AG, who I’m told has pulled in the CO Dept of Revenue, which regulates dealerships and has expertise in contracts, and an auto dealership investigator and the AG’s consumer credit expert as well.

Are you considering expanding this reporting into a nationwide auto sales industry investigation?

Would be nice. I’m unpaid and normally limit myself to more local stuff. But if it got picked up by a media outlet with the resources to pursue it further, that’d be great.

If you want another ex-employees perspective I would be happy to chat. I am in utah

Thank you for doing this important work of journalism!