What’s wrong with “Medicare Advantage” plans?

11/14/2025 – I am re-publishing this article once again since it is the open enrollment period for Medicare. [Dec. 2024 […]

11/14/2025 – I am re-publishing this article once again since it is the open enrollment period for Medicare. [Dec. 2024 […]

Robert F. Kennedy, Jr. (RFK Jr.), Trump’s pick to head the Department of Health and Human Services, is working with Aaron

What caused the dense haze in the Grand Valley air a couple of days ago that obstructed scenic views of

Updated with additional information on 9/2/24 @ 9:57 a.m.- Thanks to a grant from the Biden administration’s U.S. Department of

Coloradans for Protecting Reproductive Freedom announced that it has surpassed their campaign’s goal of collecting 185,000 signatures to put Ballot

Coloradans for Protecting Reproductive Freedom (CPRF) made an appearance last weekend in Grand Junction to boost the signature-gathering effort to

Western slopers who are struggling with high cholesterol need to know about Bella Balsamic and the Pressed Olive on Main

The downtown Mesa County Public Library will host a free educational workshop on menstrual health on Saturday, January 27 from

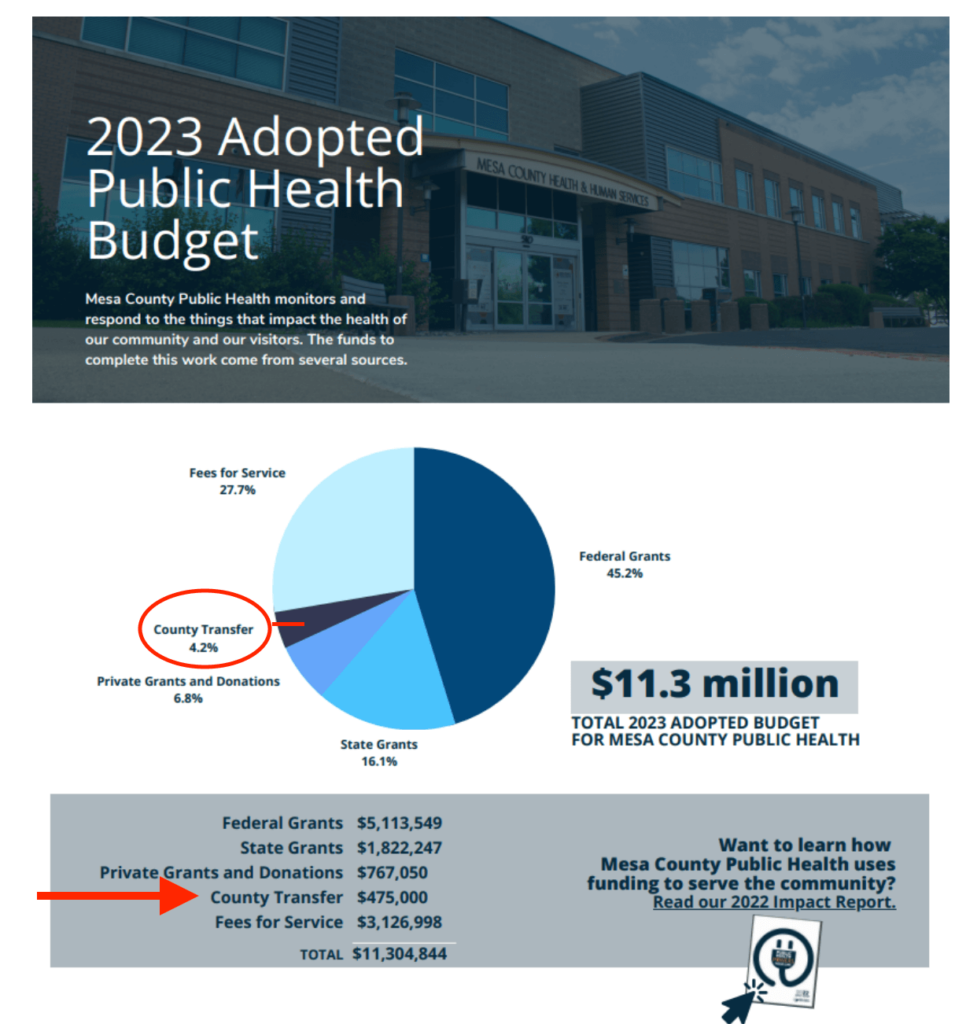

When the Mesa County Commissioners had the Board of Health (BOH) sign their new Intergovernmental Agreement (IGA), the commissioners, County

KREX reporter Michael Loggerwell’s story about Mesa County’s new Intergovernmental Agreement (IGA) with the Health Department- Part 1 KREX-TV News

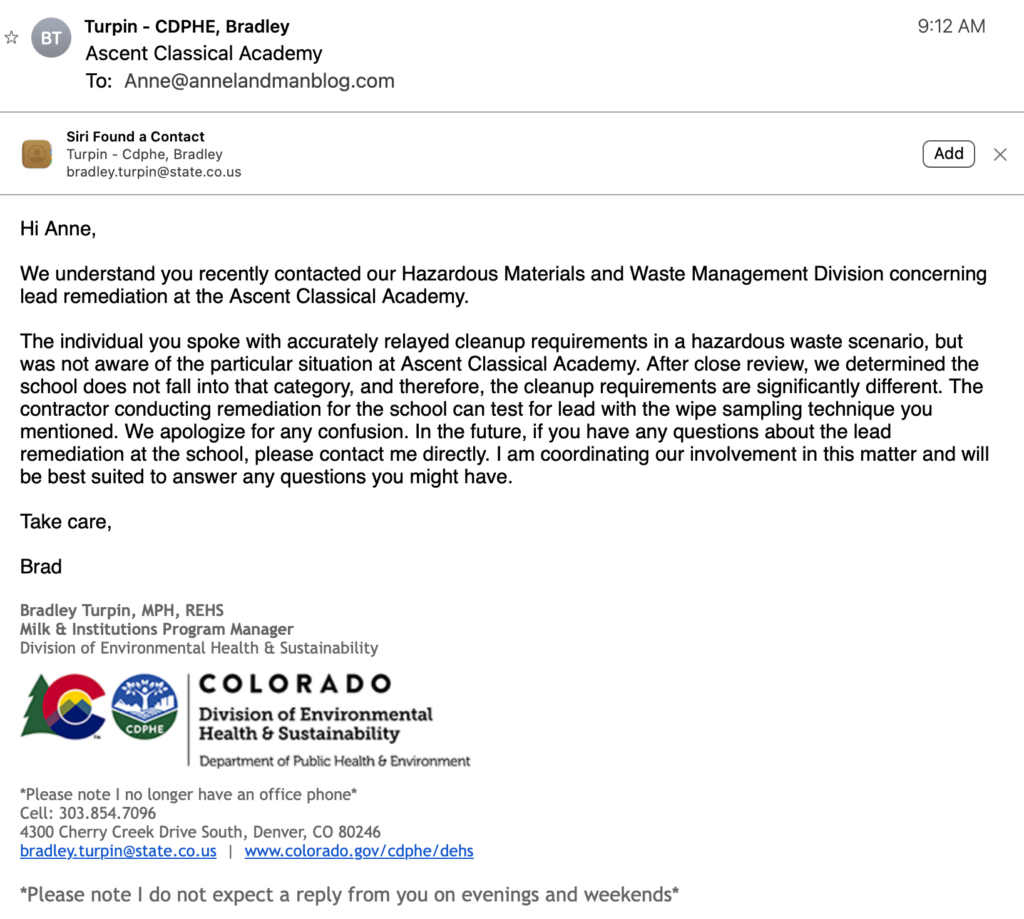

AnneLandmanBlog received the following email from Bradley Turpin, Milk and Institutions Program Manager in CDPHE’s Division of Environmental Health and

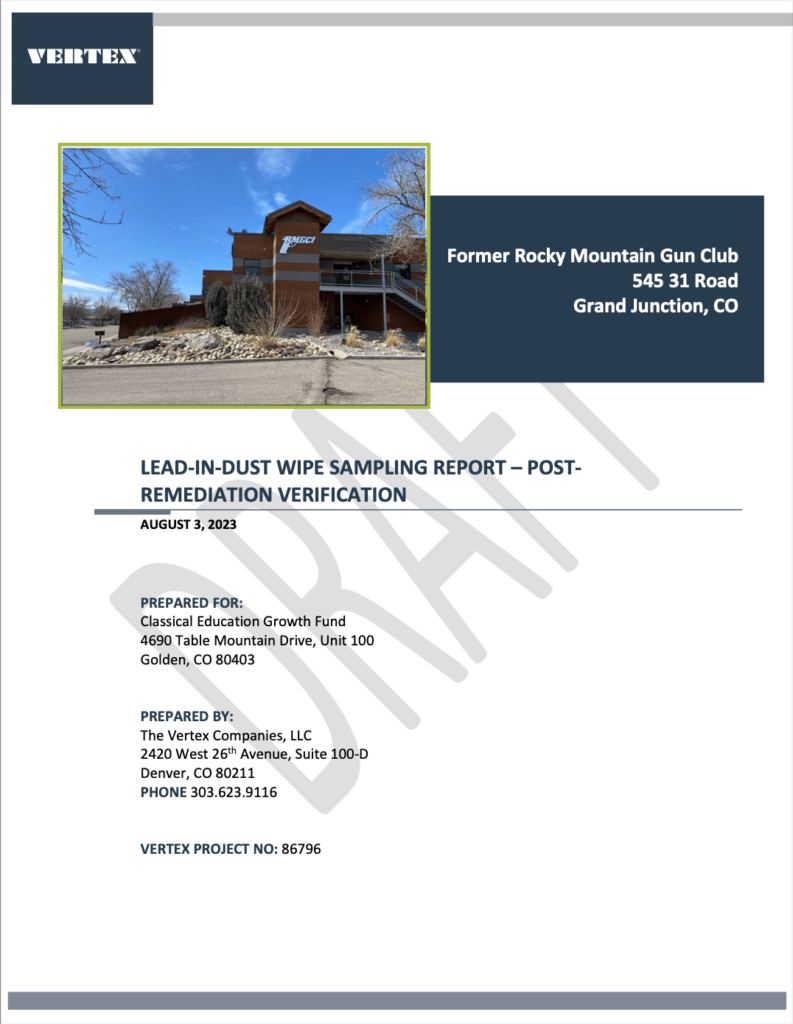

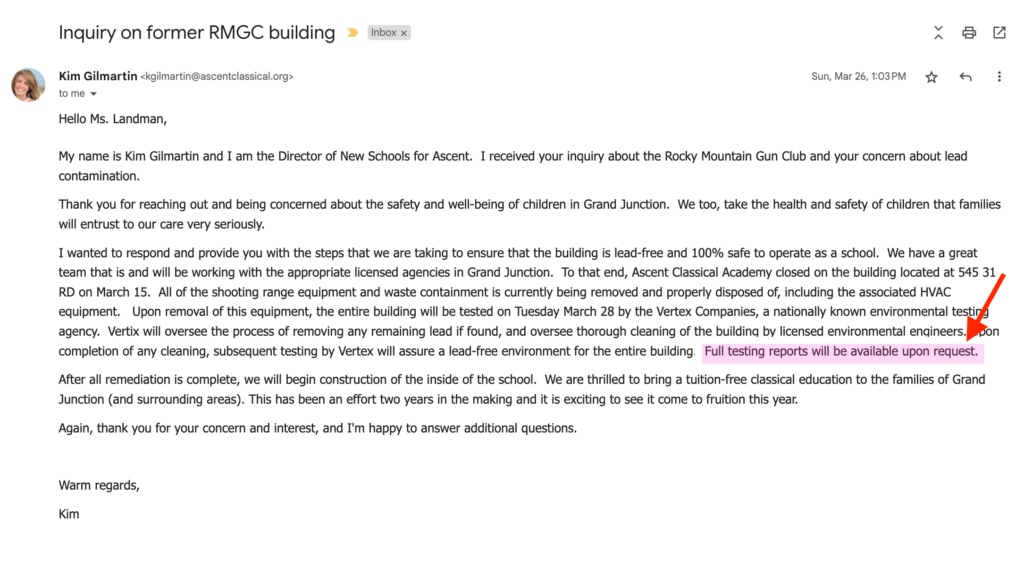

The Vertex Company LLC of Denver, which Ascent Classical Academy hired to test the old Rocky Mountain Gun Club building

Notice: Since this article was written, AnneLandmanBlog has found out from Colorado Department of Public Health and Environment (CDPHE)’s Hazardous

In the wake of Commissioner Janet Rowland’s recent coup over the Mesa County Public Health Department, if the the past

UPDATE as of 8/11/2023, 4:00 p.m. – Ascent Classical Academy updated it’s blog today with a link to a report

If Mesa County Commissioner Janet Rowland gets her way, the new, temporary members recently intstalled on the Mesa County Board

Mesa County Public Health Department (MCPHD) Director Dr. Jeff Kuhr has been under attack by the Mesa County Commissioners, who

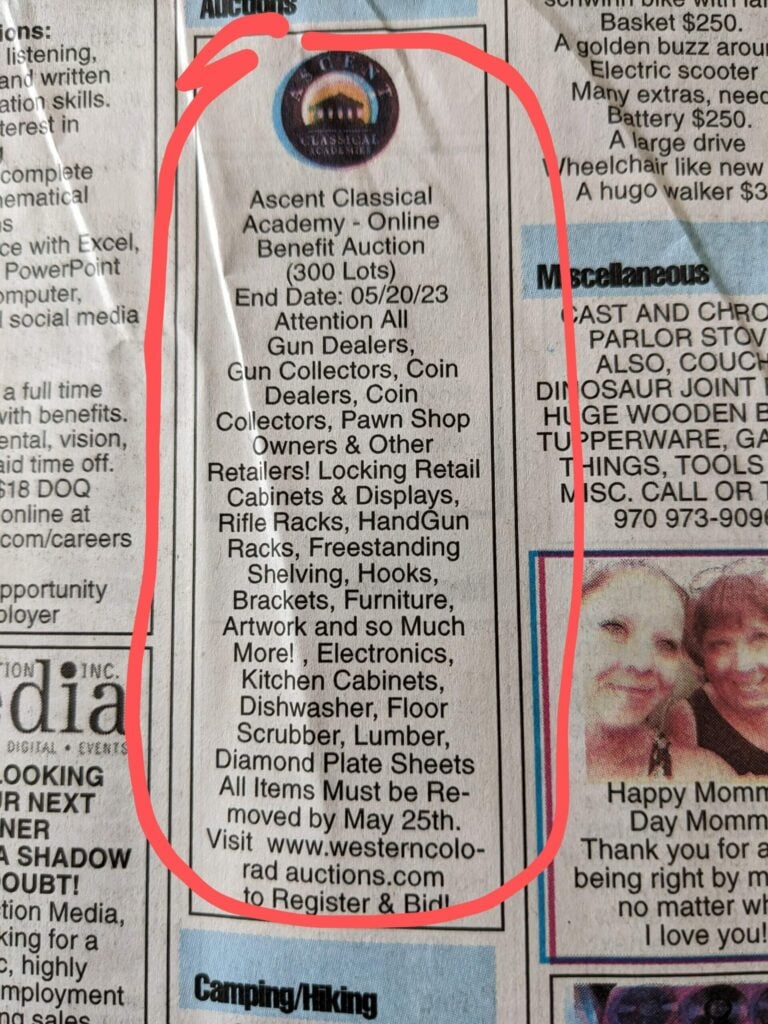

A classified ad in today’s Daily Sentinel gives notice that an auction is being held online to benefit the new